Incentives Calculator - Get an estimate of the value of Dirigo and other key tax incentive programs for your business

DECD is accepting applications for the Dirigo Business Incentives. Apply Here

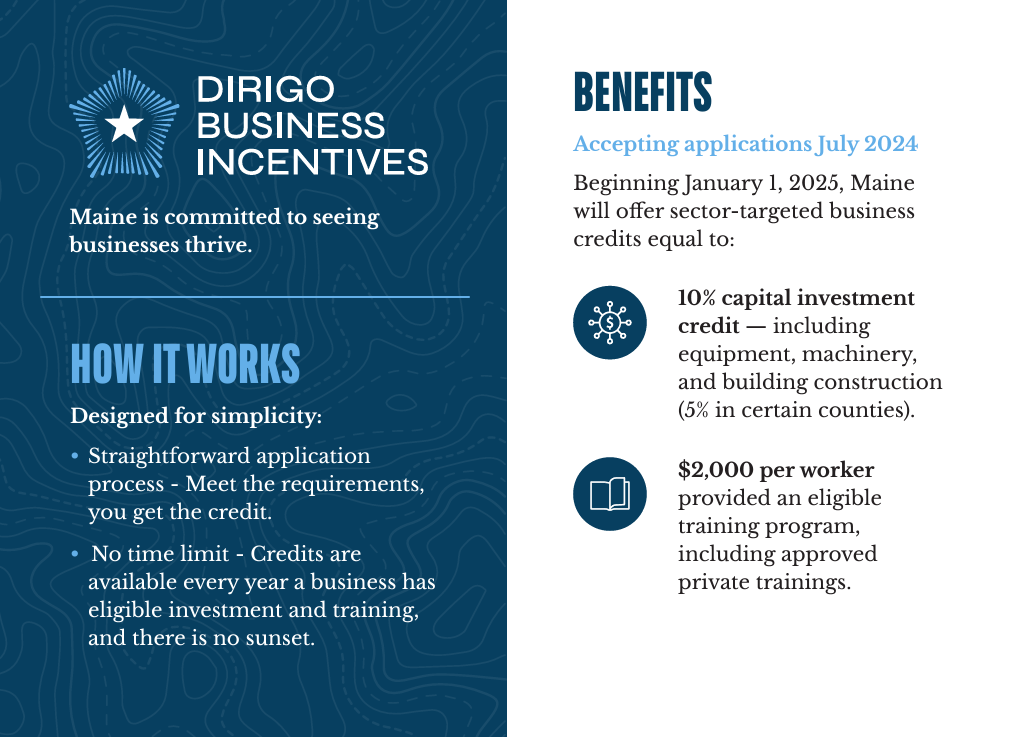

The Dirigo Business Incentives program offers eligible businesses the opportunity to greatly reduce state taxes for up to 5 years when they make significant capital investments or provide qualified employee training in certain business sectors.

Eligible sectors are:

- Agriculture, forestry and fishing

- Manufacturing

- Long-distance freight transportation

- Software publishing, data processing and computer design services

- Engineering, architecture and scientific research and development services

Benefits

- 10% capital investment tax credit (5% capital investment tax credit in Cumberland, Sagadahoc, and York counties)

- $2,000 per employee provided a qualified employee training program annually

This credit capped at $2 million per business per year and can be taken over 5 years. This credit is refundable up to $500,000 per tax year. The qualified business must claim at least $50,000 in eligible capital investment to claim annual tax credit.

Qualified Investments:

Eligible business property of the qualified business that is:

- Tangible personal property or real property (other than land)

- Purchased on or after the date of the letter of certification issued by the DECD;

- Placed in service in Maine during the taxable year beginning after December 31, 2024;

- Used exclusively in the qualified business activity described in the letter of certification; and

- Subject to an allowance of depreciation of 5 years or more, or would be subject to an allowance of depreciation of 5 years or more if the property had not been expensed under Section 179 of the Code.

Eligible business property does not include:

- Property purchased or transferred from an affiliated business;

- Property located at a retail sales facility and used primarily in a retail sales activity;

- A vehicle upon which an excise tax under 36 M.R.S., chapter 111 has been imposed;

- A watercraft upon which an excise tax under 36 M.R.S., chapter 112 has been imposed;

- Property used to calculate the credit for rehabilitation of historic properties under 36 M.R.S. § 5219-BB; or

- Real property placed in service in Maine prior to the taxable year for which the DTC under 36 M.R.S. § 5219-AAA is sought.

The business must intend to place eligible business property into service or begin training as part of a qualified worker training program within two years of filing their application for certification. Capital investment or worker training begun prior to the issuance of a letter of certification will not be eligible for the credit.

A qualified employee training program is defined as:

- An apprenticeship program registered under the Maine Apprenticeship Program

- An on-the-job training contract through a Local Workforce Board

- A training provided by or approved for funding from the Maine Community College System

- Education or training provided by the University of Maine System or other accredited university or college in this State

How to Apply

Businesses that meet the requirements of the program will receive the Dirigo Business Incentive.

DECD is now accepting applications for the Dirigo Business Incentives. Apply Here.

Rulemaking

The primary Dirigo Business Incentives statute is available here:

Title 36, §5219-AAA: Dirigo business incentives program (maine.gov)

The rule text and a summary of comments and responses received during the rulemaking process are available here:

Chapter 300: Dirigo Business Incentives Program (PDF)

Chapter 300: Dirigo Business Incentives Rulemaking Comments and Responses (PDF)

DECD Rule Making Activity – Proposed Rule

Maine Department of Economic and Community Development is proposing new Rule 301 (“Dirigo Business Incentives Tax Credit”) to implement the Maine income tax credit recently enacted by P.L. 2023, c. 412, Pt. J, § 13. The credit, found in the law at 36 M.R.S. § 5219-AAA, applies to tax years beginning on or after January 1, 2025. The refundable credit (subject to limitations) is based on a combination of expenditures to purchase eligible business property and to train qualified employees for a qualified business activity carried on primarily in an eligible sector. The Department of Economic and Community Development (DECD) is jointly proposing this rule with Maine Revenue Services, which is proposing this same rule under DAFS Chapter 816.

The proposed rule is available here: April 2, 2025 (Word)

Comments on proposed Rule 301 are due by May 5, 2025, and must be directed to Shae McGehee, Economic Development Incentive Manager, either by email at shae.mcgehee@maine.gov or by mail at Maine Department of Economic and Community Development, 59 State House Station, Augusta, ME 04333

Please note that the Pine Tree Development Zone (PTDZ) and Employment Tax Increment Financing (ETIF) programs closed for new applications on December 31, 2024.